Fleet Insurance Bundles: Cost Review

The cheapest fleet cover is often not the lowest quote — choose bundles that cut downtime, claims and admin to lower full-year costs.

If I had to cut this article down to one point, it would be this: the cheapest fleet cover is often not the lowest quote. For many UK fleets with 3+ vehicles, a single fleet policy can trim premiums by around 10–30%, but the total yearly bill also depends on downtime, excesses, claims admin, legal disputes, and add-on costs.

If I were reviewing bundle options, I’d judge them on five things:

- Starting premium

- Add-on cost

- Admin time

- Claims and downtime cost

- Renewal effect after 12 months

Here’s the short version:

- Single fleet policy often suits fleets with 3 or more vehicles and can cut admin with one renewal date.

- Breakdown and courtesy vehicle cover can make sense when a van off the road means lost jobs or missed deliveries.

- Legal and excess protection can help when a fleet deals with repeat small claims, disputed blame, or high excess payments.

- Insurer-run claims handling can lower internal workload and help keep claim delays from adding cost.

- Telematics-backed cover can shift renewal pricing, with figures in the article pointing to 5–15% day-one discounts, 10–25% lower renewal premiums, and 15–30% fewer claims where driving data is used well.

The main test is simple: which bundle cuts your biggest cost problem? If your biggest issue is paperwork, one fleet policy may do enough. If it is vehicles sitting idle, breakdown and courtesy cover may earn their keep. If it is claim frequency or theft, telematics may change the maths.

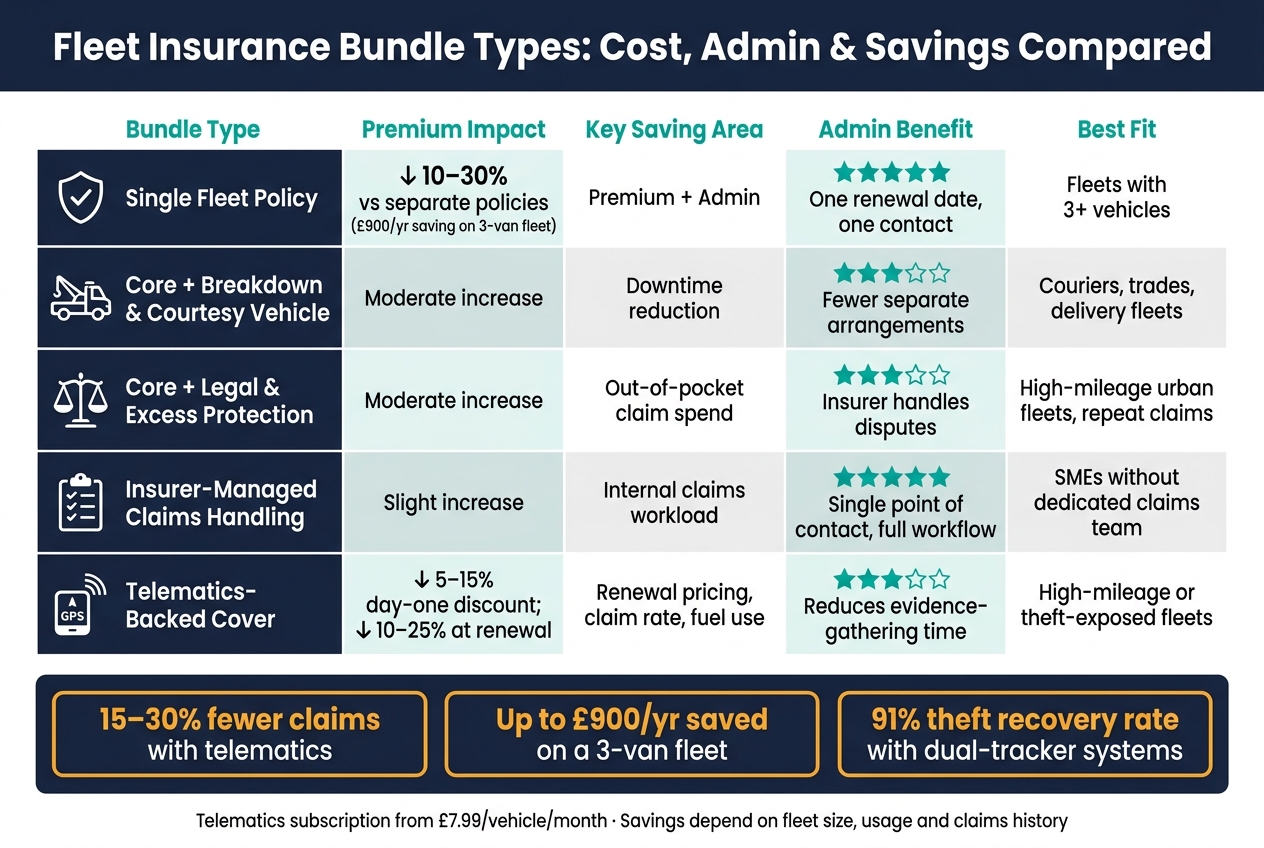

Fleet Insurance Bundle Types: Cost, Admin & Savings Compared

Quick Comparison

| Bundle type | Upfront cost | Main saving area | Best match |

|---|---|---|---|

| Single fleet policy | Lower in many cases | Premium + admin time | Fleets with 3+ vehicles |

| Core + breakdown/courtesy | Higher | Downtime | Delivery, trades, service visits |

| Core + legal/excess | Higher | Out-of-pocket claim spend | Fleets with repeat claims or high excess |

| Insurer-managed claims | Slightly higher | Internal claims workload | Firms without a dedicated fleet claims process |

| Telematics-backed cover | Device/subscription cost from £7.99 per vehicle/month | Renewal pricing, claim rate, fuel use | High-mileage or theft-exposed fleets |

So if I were comparing bundles, I would not ask, “Which quote is lowest?” I would ask, “Which option leaves me with the lowest full-year cost once delays, claims and admin are included?”

sbb-itb-499a7f0

1. Single Fleet Policy vs Separate Vehicle Policies

Total Spend

For most UK firms with three or more vehicles, a single fleet policy will usually come out cheaper overall. Insurers use fleet rating, which means they spread risk across all vehicles and drivers. In plain English, they look at the fleet as a whole instead of pricing each vehicle on its own. That pooled model can cut total motor premiums by about 10–30% for fleets with three or more vehicles.

The gap can be pretty clear in pounds and pence. A 3-van fleet on one policy costs about £1,800–£2,100 a year, compared with roughly £2,400–£3,000 for three separate business van policies. That’s a saving of up to £900 per year. Move up to a 15-vehicle mixed fleet with 10 vans and 5 cars, and the difference gets bigger: separate policies may total around £15,000 a year, while a fleet policy could cut that to about £13,900.

That said, separate policies can still work well in one specific case: when one vehicle brings much more risk than the rest. Think of a specialist HGV or a van with a poor claims record. If that vehicle sits inside the fleet policy, it can push up the rate for everything else. Keeping it on its own policy while grouping the other vehicles can help protect the fleet price.

Admin Load

Admin matters just as much as the headline premium. A single fleet policy gives you one renewal date, one schedule, one set of documents and one point of contact for changes. That’s simpler. It also means less back-and-forth every time you add, remove or update a vehicle.

With separate policies, each change has to be handled policy by policy. That takes more time and leaves more room for slip-ups, like a missed renewal or cover that doesn’t quite match across the fleet.

For many firms, that admin saving starts to justify grouping vehicles once you get to five or more.

Claims Cost

Under a fleet policy, claims are judged on overall fleet performance. The insurer looks at the fleet’s total claim frequency and severity instead of treating every incident as a stand-alone event. So one small bump or scrape is less likely to hit your premium as hard as it might under an individual vehicle policy.

Fleet policies also tend to include a more organised claims setup. That can mean dedicated fleet claims teams, agreed repair networks and standard excess terms. If your business loses money when a vehicle is off the road, that matters. A missed delivery slot or a delayed job can cost more than the repair itself, so a smoother claims process can trim the hidden cost as well as the direct one.

Pricing Impact

Fleet underwriters like steady risk control. Better fleet-wide risk data can shape renewal pricing in your favour. Driver training, licence checks, incident reporting and telematics all feed into how an insurer judges your fleet at renewal.

That’s one of the big differences with a fleet setup. Because the risk is pooled, good habits across the whole fleet can help the next price you’re offered. With separate policies, that effect is much more patchy because each vehicle is priced on its own history and renewal cycle.

The main case where a stand-alone policy still makes sense is when one high-risk vehicle would push up the rate for the rest of the fleet. In that situation, keeping that vehicle separate while moving the others onto one fleet policy can protect the fleet rate.

| Factor | Separate Vehicle Policies | Single Fleet Policy |

|---|---|---|

| Annual cost (3 vans) | £2,400–£3,000 | £1,800–£2,100 |

| Renewal management | Multiple staggered dates | One annual renewal |

| Mid-term changes | Per-policy, per-insurer | Single broker contact |

| Claims assessment | Per-vehicle basis | Aggregate fleet level |

| Risk management rewards | Fragmented, uneven | Fleet-wide pricing benefits |

That base saving is only the starting point. Add-ons can shift the total spend quite a bit, especially when downtime and claims costs come into play.

2. Core Fleet Policy with Breakdown and Courtesy Vehicle Add-Ons

Total Spend

Once your fleet sits on one policy, the add-ons start to do the heavy lifting. Breakdown assistance and courtesy vehicle cover will push the premium up. But that extra spend can still pay off if it cuts downtime by enough to more than cover the increase.

The key point is simple: the maths depends on what an hour off the road costs your business. If one missed delivery, delayed engineer visit, or cancelled job burns through more money than the add-on costs, the policy may save money overall.

The next part is less about premium and more about whether admin and claims handling get easier too.

Admin Load

Putting these add-ons under the same policy trims the number of moving parts. Instead of dealing with one recovery provider and a separate replacement vehicle setup, both sit under the same policy terms.

That means fewer separate arrangements for a fleet manager to track, update, and chase. In day-to-day use, that can make incident handling feel a lot less messy.

Claims Cost

The main gain here is lower downtime cost, not just extra cover on paper. Breakdown assistance can help get a vehicle recovered sooner. Courtesy vehicle cover can limit the knock-on cost of a vehicle being off the road while repairs are carried out.

For some fleets, that's where the money is. A delayed job or missed delivery slot can cost more than the repair bill itself, so the saving comes from cutting the time a vehicle is unavailable.

Policy wording matters. In particular, check:

- replacement vehicle limits

- call-out terms

- excess exposure

Those points shape what is covered and how much the business ends up paying when a claim happens.

That lower disruption only helps at renewal if the premium uplift stays below the value of the downtime saved.

Pricing Impact

Renewal pricing goes up with these add-ons, but net cost can still come down if they prevent enough downtime. In plain English, you pay more for the policy, but you may spend less overall if breakdowns happen often or repairs create costly delays.

| Cost Category | Unbundled cost | Bundled effect |

|---|---|---|

| Breakdown assistance | Arranged separately | Included as an add-on to the core policy |

| Courtesy vehicle cover | Arranged separately | Included under the policy terms |

| Admin and incident handling | Split across multiple arrangements | One recovery and replacement process |

3. Core Fleet Policy with Legal Protection and Excess Protection Add-Ons

Total Spend

Breakdown cover helps keep vehicles moving. Legal and excess protection deal with something else: the cost of the claim itself.

Yes, these add-ons push the premium up. But when smaller claims happen often, they can cut overall spend by lowering what the business has to pay out after each incident.

Admin Load

Legal protection can take a fair bit off the team’s plate. Instead of your staff chasing uninsured losses or dealing with disputes, the insurer handles that work. That means less back-and-forth and less need for in-house legal help.

Claims Cost

Excess protection softens the blow of repeated excess payments. Legal protection can also help the business recover uninsured losses from third parties.

And there’s a catch. Without video evidence, claim disputes rise sharply.

Pricing Impact

| Cost Category | Without Add-Ons | With Add-Ons |

|---|---|---|

| Uninsured loss recovery | Business handles it | Insurer handles it |

| Per-claim excess payments | Paid by the business | Reimbursed under cover |

| Dispute handling | Handled in-house | Handled by insurer |

The next step is pricing risk with more precision. That’s where tracker-backed data starts to matter.

4. Bundled Fleet Cover with Insurer-Managed Claims Handling

Some fleet policies cover more than the policy itself. They also include claims handling.

That means once a claim is reported, the insurer runs the process in one place. They sort repairs, recovery and third-party correspondence from first notification through to settlement. The premium is usually higher, but overall spend can drop if this setup cuts delays, back-and-forth and disputes. After that, the next lever is data, where telematics can affect how insurers price risk.

Total Spend

One claim can hit your budget from several angles at the same time. You might be dealing with repair bills, recovery charges, third-party damage and downtime all at once.

When claims handling sits in one central process, it can cut duplicated delays across those cost areas. That matters, because the longer a claim drags on, the more extra cost tends to build around it.

Admin Load

The insurer takes over the claims workflow from the first report through to settlement. That includes handling repairs, recovery and third-party correspondence directly.

For a fleet manager, that can take a lot of the day-to-day pressure out of the process. Instead of chasing several parties, you have one route for updates and decisions.

Claims Cost

Prompt first notification of loss helps keep delay costs down. It can also reduce third-party costs, especially when issues are dealt with before they snowball.

In plain terms, speed matters. A claim reported early is often easier to control than one left sitting for days.

Pricing Impact

Centralised claims handling can ease renewal pressure by getting claims closed sooner. But there’s a trade-off: the insurer has more control over repairs and settlements.

That sets up the next bundle type: telematics-backed cover.

| Cost Category | Estimated Expense Range |

|---|---|

| Vehicle Repair/Replacement | £3,000 – £45,000+ |

| Third-Party Property Damage | £8,500 (average) |

| Recovery and downtime | £500 – £2,000 recovery; £150 – £400 per day downtime |

| Replacement transport | £40 – £80 per day |

| Legal Fees (Contested) | £2,000 – £15,000 |

| Insurance Premium Increase | 15% – 35% (over 3–5 years) |

5. Fleet Cover with Telematics-Backed Risk Data

Where insurer-managed claims handling helps keep costs down after an incident, telematics-backed cover aims to cut risk before anything goes wrong. That changes the conversation at renewal too. Claims handling reacts to loss; telematics helps prevent it, then gives you hard data to support your case when pricing comes up again.

Total Spend

Fleets using telematics-backed cover often see 10–25% lower renewal premiums and 15–30% fewer claims. On top of that, telematics can trim fuel spend by 5–15% and help reduce wear from rougher driving.

Set that against a GRS Fleet Telematics tracking subscription at £7.99 per vehicle per month, and the maths can swing in your favour within the first renewal cycle.

Admin Load

Telematics can ease claims admin, but it doesn't remove admin altogether. It cuts down the manual work involved in piecing incidents together by recording time-stamped location and event data. That means less internal time spent building an evidence file.

The catch? You take on data oversight, driver briefings and regular scorecard checks. Fleets that install the system and then leave it alone usually don't get the best return. The data needs attention. Regular driver reviews and feedback are what turn raw tracking data into fewer claims and better renewal pricing.

That admin saving only works when the data is actively reviewed.

Claims Cost

Telematics and dashcam data give insurers direct evidence on speed, location and driver inputs. That matters when liability is disputed or when decisions need to be made fast.

Camera-plus-telematics products have been shown to cut claims frequency by 17% and claims costs by 36% over three years, largely because they speed up liability decisions and reduce disputes. Dual-tracker systems, including GRS Fleet Telematics, also help with theft recovery. GRS reports a 91% recovery rate.

Pricing Impact

Insurers don't price telematics as a simple yes-or-no feature. They look at it in layers.

An approved device can bring a 5–15% day-one discount. Then, at renewal, insurers review patterns such as speeding, harsh braking, night driving and driver scorecards to decide whether the fleet merits more discount or a premium loading.

This is the key point: insurers price patterns, not one-off events. A fleet that can show around a 20% reduction in harsh braking events and steady improvement in driver scorecards over 12 months has a much stronger hand in renewal talks. Fleets without solid data are more often ending up on the back foot, facing higher base premiums and tighter terms.

The same data that helps cut claims also shapes renewal terms. Better data lowers the odds of a loading and gives the fleet more weight in negotiation.

| Cost Category | Standard Bundled Policy | Telematics-Backed Bundle |

|---|---|---|

| Premium at renewal | Based on claims history and fleet profile | Up to 25% lower with proven safer driving |

| Day-one discount | None | 5–15% for fitting approved device |

| Claims frequency | Unmanaged | 15–30%+ reduction with driver coaching |

| Claims cost per incident | Standard | Up to 36% lower over 3 years |

| Fuel spend | Unaffected by cover type | 5–15% reduction from behaviour change |

| Telematics subscription | None | From ~£7.99 per vehicle per month |

Pros and Cons of Each Bundle Type

The table below shows a simple truth: some bundle types cut spend, while others mainly move cost from the insurance premium into downtime, admin, or claims work.

| Bundle Type | Principal Advantages | Principal Drawbacks | Best Suited For |

|---|---|---|---|

| Single Fleet Policy | One renewal date; multi-vehicle discounts; significantly less admin than separate policies | One high-risk driver or vehicle can affect the whole fleet's pricing; higher minimum premiums can be a poor fit for micro-fleets | Medium to large fleets with five or more vehicles, especially logistics, construction, utilities or field services |

| Breakdown & Courtesy Vehicle Add-Ons | Reduces downtime for jobs that depend on vehicle uptime; keeps drivers moving after an incident | Can duplicate existing manufacturer or business breakdown cover; courtesy vehicle limits can leave gaps; adds to premium | Couriers, service engineers and trades where a vehicle off the road means lost revenue |

| Legal & Excess Protection Add-Ons | Covers legal costs and uninsured losses; refunds policy excesses; can smooth cash flow when several claims land close together | Adds premium spend that low-claim fleets may not recoup; excess protection can have annual caps and exclusions | High-mileage urban fleets, fleets with several drivers or fleets running a higher excess |

| Insurer-Managed Claims Handling | Single point of contact; faster first notification of loss; reduces in-house claims admin | Less control over repair network and timelines; insurer priorities may not match operational urgency | Growing SMEs without a dedicated claims team; mid-size regional operators moving to structured fleet cover |

| Telematics-Backed Cover | Day-one premium discounts of about 5–15%, with further savings at renewal for fleets that improve driver behaviour | Ongoing telematics costs, including GRS Fleet Telematics from £7.99 per vehicle per month, plus the need for regular data review and driver coaching | High-mileage van fleets, fleets with variable driver behaviour or fleets where theft risk and accident frequency are major cost drivers |

For fleets with five or more vehicles, a single fleet policy is usually the starting point. It cuts admin, lines up renewals, and often gives access to multi-vehicle discounts. But the cheapest-looking option on paper isn't always the one that saves the most over a year.

In practice, the best bundle is the one that attacks your biggest cost pressure. For some fleets, that's downtime. For others, it's claims hassle. And for busy teams, it may just be the time lost chasing renewals and paperwork.

That’s why each add-on needs a proper sense check against what you already have. If the fleet is already covered by manufacturer breakdown support or an existing business contract, paying again through a bundle may not do much for you.

Telematics-backed cover can work well, but only if the business uses the data. Review driver behaviour often, coach where needed, and insurers may look more favourably at renewal. It can also help when theft risk and accident frequency are pushing costs up. If nobody reviews the reports, though, the saving tends to fade.

Total Spend Summary and Verdict

The table below compares premium, add-ons, admin, claims handling and telematics costs across each bundle type. That gives you a much clearer net-cost view than looking at premium alone.

| Bundle Type | Premium trend | Add-On Cost Effect | Admin saving | Telematics Cost | Best fit |

|---|---|---|---|---|---|

| Single Fleet Policy | Usually the lowest-admin option for fleets of three or more vehicles | None | High - low admin overhead | £0 | Strong value once admin is included |

| Core + Breakdown & Courtesy Vehicle | Moderate increase | Moderate - raises upfront spend | Low | £0 | Cost-effective when vehicle downtime is business-critical |

| Core + Legal & Excess Protection | Moderate increase | Moderate - adds another premium layer | Low to medium | £0 | Worth considering where disputed liability, uninsured losses or repeated excesses are more likely |

| Insurer-Managed Claims Handling | Slight increase | Low | Very high - reduces internal labour and repair-chasing | £0 | Best for larger fleets or businesses without an in-house claims team |

| Telematics-Backed Cover | Can fall when risk data is strong | Low to moderate | Medium | From £7.99 per vehicle/month | Strong for high-mileage or theft-exposed fleets that actively use the data |

The main point isn't which bundle looks cheapest at first glance. It's which one removes the biggest hidden cost.

No bundle works best for every fleet. Add-ons push up the premium, but they can still save money overall when downtime, legal disputes or repeated excess payments would cost the business more than the extra cover. Telematics-backed cover can shift the maths too. It may support risk-based pricing and help cut claims frequency, theft risk and vehicle misuse, but that only happens if the data is used day in, day out.

Bundling cuts spend when it lines up with the fleet's main cost driver, such as admin, downtime, disputes or risk data. A simpler policy often gives better value when the fleet is small, claims are rare, and extra cover adds cost without cutting losses.

FAQs

When should I switch to a fleet policy?

Consider switching when individual cover no longer fits the job of managing more than one vehicle. That often happens when renewal dates don’t line up, paperwork starts piling up, or your current setup gives you less control over risk than you need.

A fleet policy can make even more sense if you use telematics. In many cases, insurers look at real-time driver behaviour, not just fixed details on paper. Before you switch, check that your telematics setup meets the insurer’s requirements. If it doesn’t, your cover or any discount linked to it may not stay in place.

Which add-ons are actually worth paying for?

Focus on add-ons that lower risk and make claims less of a headache. Insurance-approved telematics, especially Thatcham S5 or S7 trackers, can be a must-have for comprehensive cover and may help you get a lower premium. Dual-tracker systems add another layer of security and can also help bring down theft-related premiums.

AI-powered dashcams and tools that support usage-based insurance are worth a look too. They can give you clear claims evidence and driving behaviour data, which may help with long-term cost control.

How long does telematics take to reduce insurance costs?

Telematics can cut insurance costs from day one if an approved device qualifies for an upfront premium discount.

After that, the savings often build over time, usually at renewal, when insurers review your fleet’s driving data. If drivers are safer on the road and incidents drop over the months ahead, that can help support lower premiums.